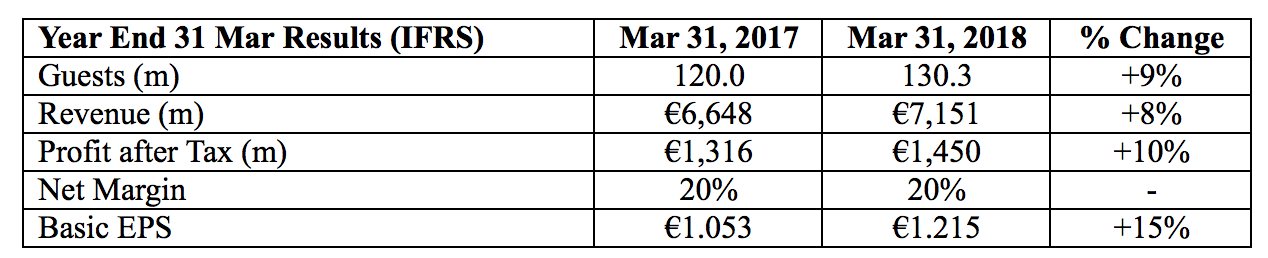

Ryanair today (21 May) reported a 10% increase in full year profit after tax to €1.45bn, as lower fares (down 3%) stimulated 9% traffic growth to over 130m guests, and an industry leading 95% load factor.

Ryanair’s CEO Michael O’Leary said:

“We are pleased to report a 10% increase in profits, with an unchanged net margin of 20%, despite a 3% cut in air fares, during a year of overcapacity in Europe, leading to a weaker fare environment, rising fuel prices, and the recovery from our Sept. 2017 rostering management failure. Highlights of the last year include:

Traffic grew 9% to over 130m, despite grounding 25 winter aircraft

Average fare fell 3% to just €39.40

Unit costs were cut by 1% (ex-fuel they rose +3%)

Ryanair Labs stimulated record ancillary spend (+4% per guest)

We took delivery of 50 B737 aircraft, bringing the fleet to 430 units

We created 1,500 new jobs, and over 600 promotions

New 5 year pay deals were concluded with most of our pilots and cabin crew

Over €800m was returned to shareholders via buybacks

We recovered quickly from the Sept. 2017 pilot rostering failure

Sales:

Average fares last year declined by 3%, which was good news for our guests but bad news for competitors. Traffic grew 9% to over 130m with Germany, Italy and Spain being our 3 largest growth markets. We expect above average EU capacity growth to continue into FY19, which will have a downward effect on fares. This may be partly ameliorated by the switch of some charter capacity back to previously security challenged markets such as Turkey and Egypt. We expect later in the year, some upward pressure on pricing as significantly higher oil prices impact margins, especially those EU airlines who continue to expand despite having no prospect of achieving profitability. Ryanair will continue to pursue our load factor active/yield passive strategy. No other EU airline can compete with Ryanair’s prices.

During FY18 we took delivery of 50 new B737s, and increased our Boeing order to 135 firm MAX-200 Gamechangers, with a further 75 under option (210 in total). We opened 4 bases in Burgas, Memmingen, Naples & Poznan and launched over 260 new routes. This summer, we have announced over 200 new routes including markets in Jordan, Turkey and the Ukraine. We continue to grow strongly in Germany, Italy and the UK, and our Polish charter airline, Ryanair Sun, operated its first flights in April 2018.

Ancillaries, Labs & Customer Service:

Ryanair Labs continues to deliver improvements in Customer Service, mobile & digital platforms, and our ancillary sales conversions. Labs has established 3 development offices in Dublin, Wroclaw, and Madrid, and employs almost 600 highly skilled digital professionals.

“MyRyanair” membership has grown to 43m, while our website & app has over 1 billion visits p.a. Our improved mobile and digital platforms have delivered a 13% increase in ancillary revenues (+4% per guest) to over €2bn. Ancillaries now deliver 28% of revenue and we are well on track to achieve our 5 year goal of 30%. More guests are switching to our great value “plus” fares, reserved seating, priority boarding, and car hire. Ryanair Rooms penetration is rising steadily, albeit from a low base, as our guests recognise our unique combination of lowest hotel prices and travel credits.

In the area of Customer Service, we have lowered our checked bag fees while increasing the bag allowance (to 20kg). Our amended 2 cabin bag policy (1 of which goes in the hold f.o.c. for non-priority guests) has improved boarding and punctuality, and we are expanding our offers in areas such as FastTrack, and ground transport connections. In March we launched our new environmental policy, which commits Ryanair to a series of industry leading environmental targets, including moving to “plastic free” within 5 years, while allowing our guests to contribute voluntarily to our carbon offset programme, the proceeds of which will be applied to support selected environmental projects.

Over the last year our on-time performance has declined by 2% from 88% to 86%. All of this decline was accounted for by increased ATC delays due to strikes and staffing/capacity shortages mainly in France, Germany and Italy. The delivery of ATC services in Europe is lamentable and creating unacceptable delays for our customers. Punctuality in Q4 was negatively impacted by unusually adverse weather conditions, which led to multiple airport snow closures at key bases including Dublin and Stansted for a number of days in late February/early March. We are working hard to increase staffing at our larger bases, re-designing boarding procedures, and providing additional spare aircraft in S.18 to improve our punctuality to our 90% target, which is a key AGB target for the coming year.

Costs:

Ryanair enjoys a significant cost advantage over all other EU airlines, and we expect this leadership to continue. In FY18, unit costs – helped by our fuel hedging – fell 1%. Even as traffic grew 9%, ex-fuel unit costs rose 3% mainly due to one-off EU261 costs arising from our Sept. 2017 cancellations, and higher H2 staff costs as we agreed substantial pay increases and 5 year pay deals with our pilots and cabin crew. We expect the market for experienced pilots in Europe to remain tight for the next 12 months, and accordingly, this will continue to put upward pressure on staff costs for all EU airlines.

In FY19 we will invest substantially in our people, our systems, and our business as we scale up the operation to take delivery of 210 Boeing Gamechanger aircraft over the next 6 years. This will lead to a modest increase in ex-fuel unit costs next year but will underpin our growth to almost 600 aircraft and 200m guests p.a. by FY24. We expect staff costs to rise by almost €200m, half of which is higher pay for our front line people and half is additional headcount for growth.

Fuel will be a major cost headwind for the next 24 months. We are currently 90% hedged for FY19 at approx. $58pbl, which is well below current spot prices of almost $80pbl. While US Shale production remains strong, world demand for oil is growing, and a number of short term political factors in Venezuela, Libya and Iran, suggests that prices will continue to be elevated for the coming year. Air fares tend to follow oil prices (as they have downwards over the last 3 years) but with a lag of up to 12 months before higher oil prices feed through to higher air fares. Accordingly, we expect unit costs over the next year to rise by 9% (ex-fuel they will increase by 6%). Thereafter, we expect the impact of the lower seat cost Boeing 737-MAX aircraft, our new lower cost 10 year engine maintenance agreement, as well as airport growth opportunities and the disposal of older aircraft, to deliver flat or slightly declining non-fuel unit costs.

Labour Cost:

While we have made a promising start in negotiations with pilot unions, including signed recognition agreements with BALPA (UK) and ANPAC (Italy), we are also making considerable progress with our cabin crew negotiations, most notably in the UK and Spain. We suffered a 1 day pilot strike in Germany (Dec. 2017), and 3 days of cabin crew strikes in Portugal (in March/April), but in all cases, the majority of our people continued to work normally so these strikes had minimal impact on our operations. Our combination of higher pay, improved rosters, and unmatched job security will, we believe, continue to make Ryanair an employer of choice in the EU airline sector. We’re welcoming hundreds of new pilots and cabin crew to Ryanair this year, including many joiners from bankrupt airlines such as Monarch and Air Berlin among others. We will continue to deal openly and fairly with our people and their unions, but we will not make concessions on pay or productivity which threatens either our low cost model or our cost leadership in Europe.

Consolidation:

The industry in Europe continues to consolidate into 5 large airline groups. In the last year, Monarch went bust, Lufthansa acquired Air Berlin, and more recently IAG made an offer to acquire loss making Norwegian. During the period, Ryanair established a Polish charter airline, Ryanair Sun, which started flying in April and looks set to trade profitably in its first 12 months of operation. In April, we acquired 24.9% of LaudaMotion, and are working to increase that stake to 75% (subject to EU merger approval) so that we can work with Niki Lauda and his team to re-launch LaudaMotion as Austria’s No.1 low fares airline, serving markets from Austria and Germany to sun destinations primarily in Spain. LaudaMotion is an attractive opportunity as it is an Airbus operator, and we are looking for opportunities to grow its Airbus fleet to 30-50 aircraft over the next 5 years. LaudaMotion has a valuable portfolio of slots at many congested airports in Germany, Vienna, and Palma de Mallorca. We believe that by investing in these separate airlines, we can build a substantial and profitable group of EU airlines under the Ryanair Holdings banner over the next 3 years, when it is likely that further M&A opportunities will arise. LaudaMotion will require almost €100m in start-up costs, and operating losses over the next 2 years in large measure due to expensive aircraft leases from Lufthansa. Once these leases expire, we expect LaudaMotion to be modestly profitable and self-sustaining as it grows its low fare offerings in Germany and Austria.

Brexit:

We remain concerned at the likely impact of a hard Brexit. While there is a general belief that an 18 month transition agreement from March 2019 to December 2020 will be implemented and further extended, it is in the best interest of our shareholders that we continue to plan for a hard Brexit in March 2019. In these circumstances, it is likely that our UK shareholders will be treated as non-EU and this could potentially affect Ryanair’s licencing and flight rights. Accordingly, in line with our Articles, we intend to restrict the voting rights of all non-EU shareholders in the event of a hard Brexit, so that we can ensure that Ryanair is majority owned and controlled by EU shareholders at all times to comply with our licences. This would result in non-EU shareholders not being able to vote on shareholder resolutions. In the meantime, we have applied for a UK AOC which we hope to receive before the end of 2018.

Balance Sheet & Cash:

Ryanair’s balance sheet remains one of the strongest in the industry. At year end, our balance sheet included 400 owned B737 aircraft, all of which were added at their net purchase price, which is a significant discount to their current market value. Ryanair continues to generate significant cash flows. In the past year, we generated over €2bn cash from operations. Despite capex of €1.5bn, and share buybacks of over €800m, year-end net debt at March 2018 was broadly flat at €283m. In Feb., the Board approved another €750m share buyback, which we expect to complete at the end of Oct. 2018. Including this buyback, Ryanair will have returned over €6bn to our shareholders since 2008. The success of our share buyback programme is demonstrated by our 15% EPS growth in FY18 at a time when profits rose 10%.

Outlook & Guidance

Our Outlook for FY19 is on the pessimistic side of cautious. We expect to grow traffic by 7% to 139m, at flat load factors of 95%. Unit costs this year will rise 9% due to higher staff and oil prices which will, when adjusted for volume growth, add more than €400m to our fuel bill. Ex-fuel unit cost will rise by up to 6% as we annualise pilot and cabin crew pay increases, and invest in our business and our systems to facilitate a 6 year growth plan to 600 aircraft and 200m guests p.a.

We have limited H1 and zero H2 fare visibility. Forward bookings are strong but pricing remains soft. Since only half of Easter fell in April, we expect a 5% fare decline in Q1 but a 4% rise in Q2 fares. While still too early to accurately forecast close-in summer bookings or H2 fares, we are cautiously guiding broadly flat average fares for FY19. Ancillary revenues will grow as penetration of customer services continues to rise. We do not expect ancillary revenue growth to fully offset higher costs and lower fares, and so we expect FY19 profits will fall to a range of €1.25bn to €1.35bn. This guidance is heavily dependent on H2 fares, a “normal” level of ATC disruptions for S.18, the absence of unforeseen security events, and no negative Brexit developments during this period.

We have not included our investment in LaudaMotion in the above outlook as any increase to a 75% share ownership remains subject to EU Competition approval. We expect approx. €100m of start-up costs, and operating losses for LaudaMotion if and or/when our proposal to take majority ownership receives regulatory approval.”