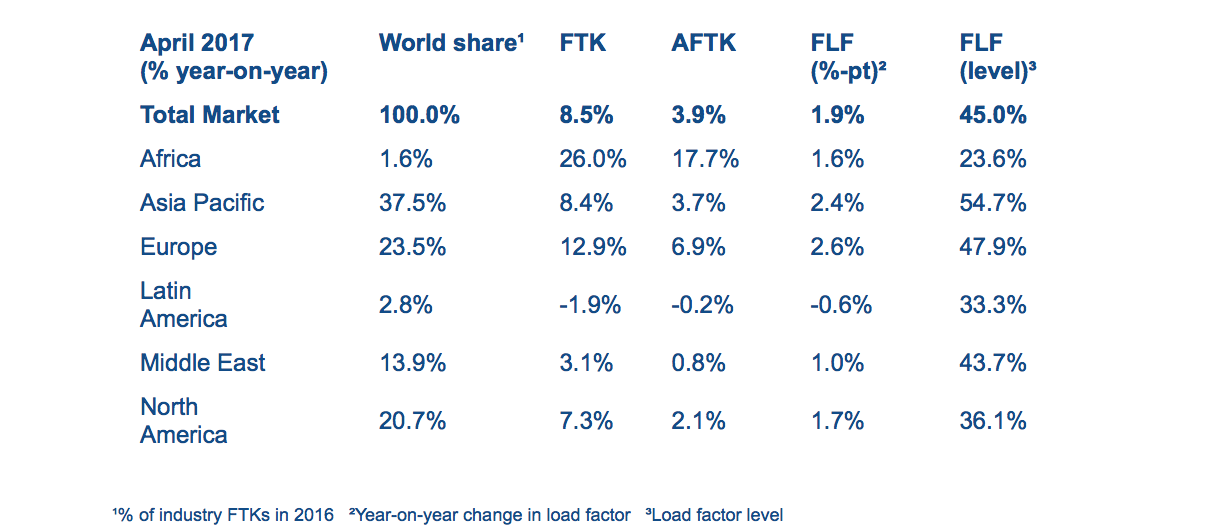

Cancun – The International Air Transport Association (IATA) released data for global air freight markets showing that demand, measured in freight tonne kilometers (FTKs), rose 8.5% in April 2017 compared to the year-earlier period. While this was down from the 13.4% year-on-year growth recorded in March 2017, it is well above the average annual growth rate of 3.5% over the past five years.

Growth in freight capacity, measured in available freight tonne kilometers (AFTKs), slowed to 3.9% in April 2017.

Business confidence indicators remain consistently upbeat, suggesting year-on-year FTK growth will remain robust for the rest of the second quarter. However, there are signs that the cyclical growth peak for air cargo has passed, particularly given that the inventory-to-sales ratio stopped falling at the end of last year. Air cargo often sees a boost in demand at the beginning of an economic upturn as companies look to restock inventories quickly. This tapers as inventories are adjusted to new demand levels. Over the whole year, air freight is headed for a healthy growth rate of 7.5%, supported by strong pharmaceuticals and e-commerce.

"Demand eased in April. Growth rates, however, are still much more robust than anything we have seen in the last six years. That’s good news, but it should not be taken as a message that all is well in air cargo. The industry’s antiquated processes need modernization. With e-air waybill utilization topping 50% in April, progress is being made. And we must harness the momentum to drive transformational change across the way the industry operates," said Alexandre de Juniac, IATA’s Director General and CEO.

Regional Performance

All regions, with the exception of Latin America, reported year-on-year increases in demand in April 2017. Airlines in Europe and Asia-Pacific accounted for more than 70% of the annual increase in global freight volumes. North American airlines accounted for much of the rest with Middle Eastern and African airlines also making a positive contribution.

Asia-Pacific airlines’ freight volumes expanded 8.4% in April 2017 compared to the same period a year earlier and capacity increased by 3.7%. The increase in volumes reflects the strength of the order books reported by exporters across the region. Seasonally-adjusted volumes recently surpassed the levels reached following the 2010 post-global financial crisis bounce-back.

North American carriers posted an increase in freight volumes of 7.3% in April 2017, and a capacity increase of 2.1%. Seasonally-adjusted volumes jumped in April, however, it is too soon to tell if this is the start of a lasting pick up. The strength of the US dollar continues to boost the inbound freight market but is keeping the export market under pressure.

European airlines posted a 12.9% increase in freight volumes in April 2017 and a capacity increase of 6.9%. This was a slight slowdown from March but still well above the five-year average of 3.5%. International freight volumes grew by 13.1% year-on-year. The ongoing weakness of the Euro persists in boosting the performance of the European freight market which has benefitted from strong export orders over the last few months.

Middle Eastern carriers’ year-on-year freight volumes increased 3.1% in April 2017. This was a sharp slowdown from the 16.3% increase in March. The drop appears to be related to volatile monthly developments last year rather than a pronounced downturn. Capacity increased 0.8%. International freight volumes increased 8.0% year-to-date in April – this is slower than the five-year average pace of growth of 11%. Seasonally-adjusted freight volumes maintained their upward trend. Demand remains strong between the Middle East and Europe but traffic to Asia has weakened.

Latin American airlines experienced a contraction in demand of 1.9% in April 2017 compared to the same period in 2016. Capacity decreased by 0.2% over the same period. Recovery in seasonally-adjusted volumes also stalled, with demand in April reaching close to a seven-year low. Demand is now 18% lower than at the peak in 2014. The region’s carriers have managed to adjust capacity, which has limited the negative impact on the load factor.

African carriers posted the largest year-on-year increase in demand of all regions in April 2017 with freight volumes growing 26%. Capacity increased by 17.7% over the same time. Demand has been boosted by very strong growth on the trade lanes to and from Asia which have increased by nearly 55% so far this year. The region’s load factor remains challenged--the lowest of all regions and well under half that of carriers based in Asia-Pacific.