London/Dublin, 4th July 20I8: As the Farnborough Air Show approaches, leading aviation consultancy IBA, analyses current trends and issues its predictions for the remainder of 2018 as part of its general market update.

Macroeconomic outlook, OEM activity, aircraft orders, fuel and lease rates are some of the key themes that IBA addresses in this month’s report. The main topics that stand out are predicted Farnborough Air Show orders as well as mid-market aircraft trends, and operator profitability.

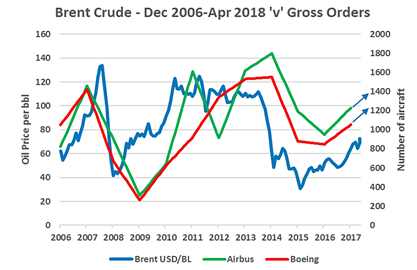

Has airline profitability peaked? According to IBA, there are mixed signals at play - positive metrics including traffic growth, vibrant new markets, and a buoyant SLB market seem to indicate that strong net profitability will continue. However, with the gathering clouds of creeping fuel prices, rising interest rates, wage inflation and increasingly price sensitive passengers, a different picture begins to emerge. Mid-2018 fuel prices are $15 higher per barrel than IATA predicted, a 40% increase year on year.

Base airfares and yields have generally stabilised since the sustained decline seen in recent years. Stronger economic conditions, leading to higher passenger demand have been offset by increased competition thereby causing base fares to be held back. IBA suggests that airline costs are expected to rise which would result in an upward trend in yields.

With the use of its airline scoring system, IBA has identified a number of airlines that are operating with negative margins and may find the times ahead particularly difficult. IBA predicts that if costs continue to rise, more airlines may begin to feel the squeeze later in the year.

IBA’s mid-market analysis indicates that there is a gap in the market in terms of pricing range and payload, however it is not clear if the gap is as large as some have estimated. Further analysis is required and IBA will continue to conduct research around the market potential for a New Midsized Aircraft (NMA).

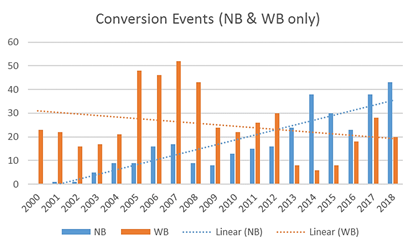

With regard to the narrow-body market, IBA expects values to remain strong for new types as demand continues to strengthen. Rising costs will favour the fuel-efficient new generation of neo and MAX aircraft, and with deliveries of new generation narrow-bodies expected to rise, an increase in retirements is also expected along with a surge in conversion demand.

As for wide-bodies, demand for mid-sized wide-body freighter conversions is strong, particularly for the Boeing 767-300ERs, which we continue to see going through the P2F process in significant numbers. Adding some future competition to this market, the first A330-300 aircraft have now been converted to freighters for DHL and the first converted A330‑200 is in testing and will subsequently enter service with Egyptair.

The Boeing 787-8 backlog continues to dwindle despite the recent orders from American Airlines. Transactions and deliveries are down and some operators have shown a desire to leave the smaller variant behind. The A380 programme benefitted from a further order from Emirates earlier this year; some transitions are apparent but teardowns have also been announced. Elsewhere, the Boeing 787-9 and Airbus A350-900 aircraft are performing well whilst mature wide-body values and lease rates are decreasing.

IBA.iQ, IBA’s data platform, forecasts over 60 Airbus A330ceo lease ends each year over the next three years while A330-200 lease ends are expected to peak in 2020, potentially pushing pricing to levels attractive for P2F conversion. IBA.iQ also forecasts a peak in Boeing 777-300ER deliveries in 2019.

With the Farnborough Air show fast approaching, IBA predicts that with a strengthening economic outlook – GDP and traffic growth, improving load factors, flattening of yield decline and rising oil prices, it is likely that we will we see strong orders for new technology during the show. IBA will continue to monitor orders as part of its Farnborough Air Show coverage which will include its pre-show predictions.