Each quarter AeroAnalysis publishes its projections for Boeing’s deferred production balance on the Boeing 787 program, which is one of Boeing’s key programs to bolster cash flows.

PAST PERFORMANCE BOEING 787

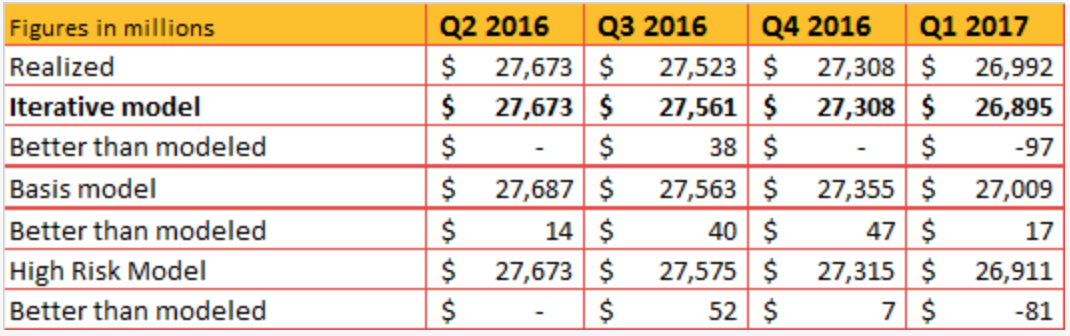

What we see is that during the first quarter the iterative model and high-risk model have been too bullish on forecasting Boeing’s ability to cut down the deferred balance, while the basis model has done quite a good job where it is just a little bit too conservative.

EXPECTATIONS Q2 2017

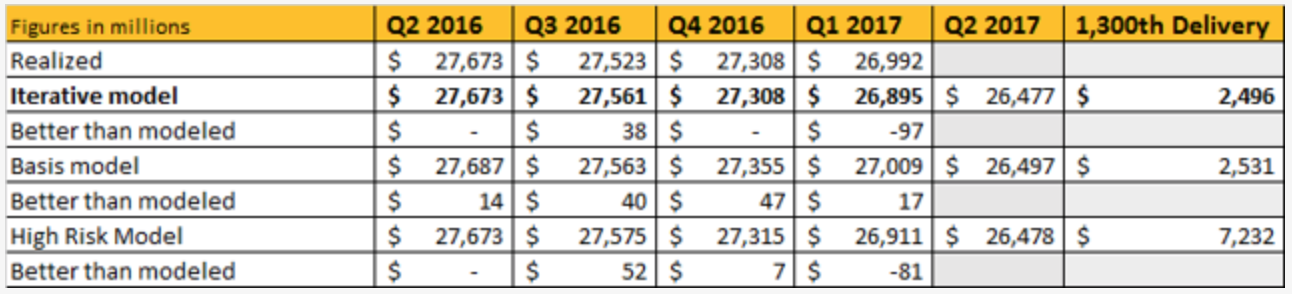

According to the 3 models that project the deferred balance over the entire accounting block, the Q2 2017 deferred balance will be slightly lower than $26.5B. On a per-unit basis the model estimates the deferred balance to decline by $15-15.6 million.

If we compare this to the projection we got from the trend of the per-unit basis improvement, we see that the model projections fall at the higher side of the $13.25-16.15 million range.

What we see is that all 3 models more or less forecast the same deferred balance for the second quarter. It should, however, be pointed out that the forecasted deferred balances at the 1,300th delivery differ significantly. The high-risk model suggests that Boeing would have $7.5B left unrecovered at the last delivery in the accounting block, while the other 2 models suggest $2.5B to be left unrecouped.

This means that currently the models point towards $6.1B-$10.8B of deferred production costs and unamortized tooling costs to be left uncovered after 1,300 deliveries.

Read the full article on Seeking Alpha

— —

Article written by partner:

AeroAnalysis was founded in June 2015 and commenced operation in July 2015. In 2013 AeroAnalysis started publishing its work on investing research platform SeekingAlpha, primarily covering the aerospace industry from a unique angle, combining knowledge about investing and aerospace products into unique write-ups that spark healthy discussions and give meaningful insight to investors.