SEPANG, 27 FEBRUARY 2018 – AirAsia Berhad (“AirAsia” or the “Group” encompassing Malaysia, Indonesia and Philippine Units) today reported its results for the quarter ended 31 December 2017 (“4Q17”) and the full financial year ended 31 December 2017 (“FY2017”).

Unaudited Consolidated Results of AirAsia Berhad

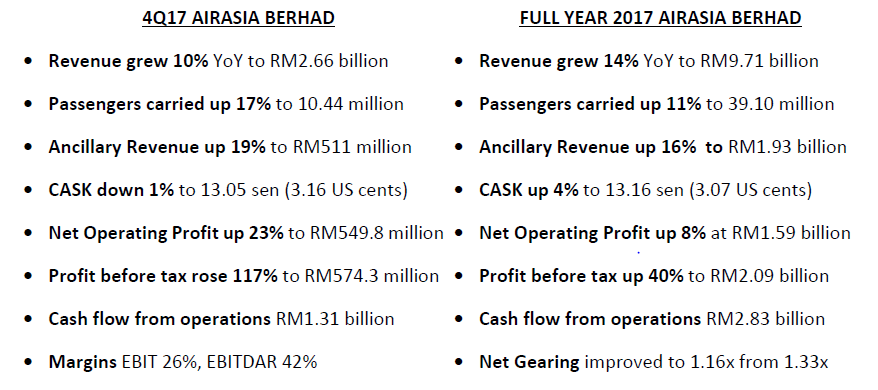

The Group posted fourth quarter 2017 revenue of RM2.66 billion, up 10% year-on-year from RM2.41 billion in the same quarter in 2016. Revenue growth was supported by very strong load factor of 88%, which was one percentage point higher and 17% increase in passengers carried to 10.44 million as compared to the same quarter last year. Net operating profit up by 14% to RM549.8 million despite higher staff, fuel and overall aircraft maintenance & overhaul expenses.

Operating cash flow stood at RM1.31 billion as compared to RM605.2 million for the third quarter 2017. The heathier cash position brings our net gearing ratio down to 1.16 times as compared to 1.33 times in 2016.

For the full financial year ended 31 December 2017, the Group posted revenue of RM9.71 billion and net operating profit, after accounting for finance costs of RM1.59 billion, up by 8% from FY2016.

Comparisons between corresponding quarters are made between the reported 4Q17 financial results and the pro forma consolidated financial results for 4Q16 detailed in note no. 22 of the quarterly statement to Bursa Malaysia prepared on similar basis as in 4Q17 where both PT Indonesia AirAsia and AirAsia Inc. Group of Companies (Philippines) results were consolidated for financial reporting purposes in accordance to MFRS 10.

Revenue Performance

Revenue per Available Seat Kilometre (“RASK”) recorded at 15.46 sen in 4Q17, marginally lower by 4% from 16.14 sen. Average fare per passenger dipped slightly to RM182 which was in line with the Group’s expectations due to rapid capacity addition of 16% year-on-year as well as the impact of the volcanic activities by Mount Agung, which disrupted our Indonesian operations in Bali for the whole of fourth quarter 2017. However, the overall impact was cushioned by the increase in ancillary revenue. The ancillary per pax grew 2% to RM49, whilst the consolidated group’s ancillary revenue grew 19% from RM429 million to RM511 million.

Thai AirAsia posted 4Q17 revenue of THB9.68 billion, up 28% from THB7.56 billion in the same quarter last year backed by a 22% increase in passengers carried. The associate company of the Group reported an increase in average fare of 6% year-on-year alongside a six percentage point increase in load factor over the same time period. Net operating profit was reported at THB786 million and net profit at THB843 million. A total of RM47 million, being the share of results of Thai AirAsia, was equity accounted into the Group’s income statement.

India AirAsia recorded a revenue of INR5.17 billion in 4Q17 from INR2.70 billion in 4Q16 and net operating profit of INR143.7 million for the quarter under review. The average fare has increased by 9%, while RASK has gone up by 16% in 4Q17 as compared to 4Q16.

Cost Performance

For the Consolidated Group, Cost per Available Seat Kilometre (“CASK”) including fuel averaged at 13.05 sen in 4Q17, marginally down 1% from 13.17 sen in 4Q16. The average fuel price for the Group was US$69 per barrel jet kerosene in 4Q17, compared to US$64 in 4Q16. CASK ex-fuel decreased by 5% year-on-year from 8.66 sen in 4Q16 to 8.26 sen in 4Q17 resulting from successful cost reduction measures on the Group’s airline-related costs namely reduction in staff costs, other operating expenses and an overall increase in other income.

Thai AirAsia reported a slight increase in CASK by 4% from 4.32 US cents in 4Q16 to 4.51 US cents in 4Q17, largely due to the rising in global fuel prices this quarter and the increase in excise tax on jet fuel consumption for domestic flights.

On the financial results for 4Q17 and FY2017, AirAsia Berhad Group CEO Tony Fernandes said:

“This past 2017 was a year of tremendous change and expansion for us. We added 30 aircraft to our group-wide fleet, of which 24 were fully operational at the close of the year. In seat capacity terms, we added 16% year-on-year in the fourth quarter and 10% for the whole of 2017. Very few of those added seats went unsold as we grew group-wide passenger traffic by 11% in FY2017, 1 percentage point more than the increase in seat capacity.”

“Our rapid expansion helped AirAsia Berhad achieve revenue growth of 10% year-on-year in the fourth quarter across our Malaysia, Indonesia and Philippine units. We successfully recorded a net operating profit at RM549.8 million up by 23% from the same quarter last year, and full year net operating profit of RM1.58 billion marginally beating the record year of 2016 by 1%. We will continue to grow our market share across our ASEAN network. We now dominate 55% of the domestic market in Malaysia, up from 47% in the same time last year. It was a remarkable quarter for AirAsia as all our ASEAN operations as well as India reported good profits.”

“Despite rapid expansion, we did not lose pricing power and only reported a small dip in average fare of 7% to RM182, as anticipated and planned for by the Group. Overall, the Group managed to draw in higher revenue growth by increasing our booking conversion rate and enticing passengers to purchase more ancillary products.”

“The Fly-Thru passengers for the Group is reported to be 1.6 million pax which is a 40% increase for the full year of 2017 as compared to the year before. Our KLIA2 hub is still the top transit hub by our passengers contributing 61% of the overall Fly-Thru traffic, and a growth of 40% from 1.1 million pax to 1.5 million pax year-on-year. We foresee higher uptake of this ancillary product as we continue to strengthen our synergy with our long haul sister company, AirAsia X Berhad.”

“On the corporate front, we announced a segregation of our businesses into airline transportation and digital divisions respectively. We are making this change to streamline our businesses, provide better clarity and business focus across each division. This new structure will also give our rising digital ventures the same prominence as our traditional airline business. Our digital businesses will continue to expand and support our airline businesses in areas such as inflight connectivity and duty free sales as well as in e-payments and loyalty. With this new structure, we are giving our digital businesses room to grow beyond serving just AirAsia and in becoming major tech players within their own right.”

“On monetisation of non-core assets, the Group completed the transaction on the disposal of our interest in our flight school joint venture with CAE and recognised a gain of RM168 million in the quarter under review. We have also concluded the ground handling joint venture with SATs and soon to conclude the sale of our aircraft leasing business, Asia Aviation Capital.”

“We are extremely proud of the turnaround by our Philippines operations. Which has proven that perseverance and our business model truly works. Despite numerous one-off costs for aircraft redeliveries, maintenance and overhaul throughout 2017, Philippines AirAsia has produced a strong bottom line recording a net operating profit of PHP621.2 million and PHP665.3 million for the full year of 2017 backed by a full year ASK growth of 37% year-on-year. We are looking forward to an exciting year leading into an IPO for our Philippines’ operations by the second half of 2018. For the full year of 2017, ancillary per pax grew 25% from PHP419 (RM36) to PHP528 (RM45). The ancillary revenue in ringgit terms have grown tremendously by 64% to RM236.6 million in FY2017 as compared to RM144.1 million in FY2016.”

“As for Indonesia, we have successfully floated AirAsia Indonesia on the Indonesia Stock Exchange on 29 December 2017 via a reverse takeover. The retail investor interest in Indonesia AirAsia has been growing ever since the airline got listed on the Indonesia Stock Exchange Market. We hope to grow the institutional investor base for our listed entity in Indonesia. Our operations in Indonesia and Philippines are attracting more interest by airline investors. The Indonesian operations recorded a net operating profit of IDR6.6 million and profit before tax of IDR75.3 million for the fourth quarter of 2017. For the full year of 2017, Indonesia AirAsia recorded a net operating profit of IDR135.7 million and profit before tax of IDR234.1 million. Taking out the one-off deferred taxations, Indonesia AirAsia would have generated a positive net profit position. Indonesia’s overall financial performance was better than expected as their operations were affected by the volcanic activities which lasted the whole of fourth quarter 2017. For 2018, we are diversifying our network in Indonesia by strengthening our key hubs in Medan and Jakarta.”

“Our Thai associate did extremely well in the fourth quarter, and aggressively closed the gap for the first 10 months of the less favourable operating environment largely due to the crackdown on the Chinese zero dollar tours and the passing of their King. A rapid recovery in tourism arrivals, boost passenger traffic growth to 22% year-on-year, much more than added seat capacity of 13%. This has led to higher average load factor of 88% for the quarter. The Chinese passengers into Thailand have risen to 9.81 million up by 12% for FY2017 as compared to FY2016. The total tourist to Thailand rose by 8.52% to 35.4 million in 2017. Thai AirAsia was the only profitable airline recording net profit of THB2.66 billion for the full year of 2017. The strong load factor for the rest of 2018 bodes well for our Thai operations.”

“Our associate airline in India has grown tremendously, achieving 79% passenger growth and 80% increase in capacity in 4Q17 as compared to 4Q16. For FY2017, passengers carried grew 81% on the back of 80% increase in capacity as compared to FY2016. We are proud to announce that our India operations have more than doubled the revenue for 4Q17 to INR5.17 billion from INR2.70 billion in 4Q16. AirAsia India has 14 aircraft as of 31 December 2017. We will be adding 7 aircraft for our India operations by the end of 2018 to fulfil the strong air travel demands. We will launch our international and regional routes with the 21st aircraft this year. We foresee AirAsia India to be very profitable once we start flying regional routes and connecting them to our already established wide network.”

“AirAsia Japan started operations on 29 October 2017, flying the route between Nagoya and Sapporo. We are targeting to start our Vietnam and China operations in the second half of 2018 after obtaining the necessary approvals.”

“We are now beginning to see the fruits of our data and digital initiatives. Our Big Loyalty’s New Membership has grown by 25% from 2.8 million in FY2016 to 3.5 million in FY2017. We believe that passengers’ data is a very valuable asset and this number will only grow exponentially as we grow our passenger numbers. The new mobile application conversion rate for flights purchased has grown 70% from 3.39% to 5.75% in FY2017. As we continue to improve our mobile application and further enhance our booking site, this conversion rate will further improve. The implementation of personalisation for ancillary from the period of October 2017 to February 2018 has improved the ancillary take up rate by 6.66%, with estimated revenue generation of USD1.7 million per month. The predictability score on ancillary uptake has contributed to an increase of 40% with the estimated revenue of USD58,366 per month. From the recently launched simplified payment enhancement, our booking conversion has increased from 7.46% to 8.57% with an estimated incremental revenue of USD30 million a month. With the full roll out of predictive data and personalisation, we foresee ancillary to be a huge revenue contributor in time come.”

On the Group’s outlook, AirAsia Group CEO Tony Fernandes said:

“Travel demand in the region is still largely unmet by the current offerings. ASEAN, Indian and Japanese travelers alike want to travel more and travel low cost. AirAsia is optimistic about the growth potential of low-cost air travel, and the potential of our fares to stimulate and grow new markets. We look to more than double our current fleet of narrowbody aircraft, now over 200-strong, to 500 fleet by 2027.”

“Our airlines are one part of the equation, while our digital businesses form another. I am glad to announce we will be consolidating our digital businesses under RedBeat Ventures and marketing to investors as an ASEAN travel and lifestyle tech ecosystem. We have got it all covered; a strong online travel lifestyle and social network presence with Travel3Sixty and Vidi, connectivity and content from Rokki as well as duty free/ merchandise from our duty free shop while inflight, and our customers can choose to go cashless with BigPay both inflight and on the ground. To tie us into e-commerce, we have just appointed Datuk Mohd Shukrie Mohd Salle, the former CEO of Pos Malaysia to head up Redbox, which is an end-to-end courier service to physically deliver your online purchases to your door step.”

“As for maximising shareholder returns, AirAsia will continue to create assets and realise the value of our investments in non-core operations as well as grow our digital and data businesses. We remain committed to a biennial distribution of special dividends from the monetisation of our non-core assets. We will soon be concluding the sale of our aircraft leasing business, Asia Aviation Capital.”

“We will continue to grow our presence and market share in the ASEAN region, with Vietnam as the final piece of the puzzle to complete our ASEAN connectivity.”

“The internal re-organisation to simplify the new group structure via changing the listing status from AirAsia Berhad to AirAsia Group Berhad is on target to complete in the second quarter of 2018. We believe that this new group structure will improve efficiency and transparency, which in time to come will help us achieve the fair valuation that reflects the true value of AirAsia.”