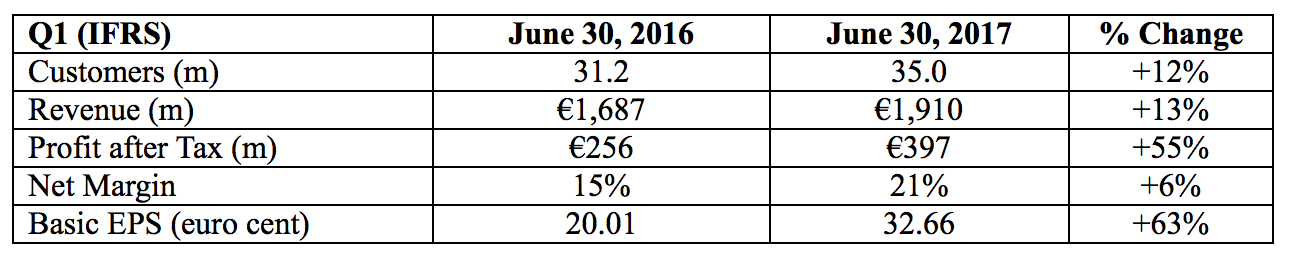

Ryanair, Europe’s No. 1 airline, today (July 24) reported a 55% rise in Q1 profit to €397m. This result is distorted by the timing of Easter in Q1 with no holiday period in the prior year comparative. Traffic grew 12% to 35m as Ryanair’s lower fares and “Always Getting Better” (AGB) programme delivered a record 96% load factor.

Ryanair’s CEO Michael O’Leary said:

“We are pleased to report this 55% increase in PAT to €397m but caution that the outcome is distorted by the absence of Easter in the prior year Q1. While Q1 ave. fares rose by 1% to just over €40, this was due to a strong April (boosted by Easter) offset by adverse sterling, lower bag revenue as more customers switch to our 2 free carry-on bag policy, and yield stimulation following a series of security events in Manchester and London. Q1 highlights include:

Traffic up 12% to 35m (LF +2% to 96%)

Ave. fare up 1% to €40.30

Unit costs down 6% (ex-fuel -3%)

10 additional B737-MAX-200 “Game Changers” ordered (now 110 firm & 100 options)

Over €200m returned to shareholders via share buybacks

397 B737’s in fleet at end of Q1

New Routes, Bases & Fleet:

We took delivery of 14 new B737’s in Q1, ahead of the peak summer period. Our new bases in Frankfurt Main (opened in March) and Naples (April) are performing well with strong advance bookings at low fares. The Frankfurt Main base will increase from 2 to 7 aircraft in Sept. We will launch 2 new bases in Memmingen (Munich) & Poznan in the autumn and open 170 new routes for winter ’17. We continue to see significant growth opportunities for Ryanair across Europe as competitors close bases or move capacity and legacy airlines restructure.

In June we ordered 10 more B737-MAX-200 “Game Changer” aircraft. Five of these will be delivered in spring 2019 and 5 more in spring 2020. In addition, we recently agreed extensions of 10 operating leases which will provide us with 3 more aircraft for S.18 and 10 for S.19. This addresses a temporary capacity shortage in S.19 (before our Boeing MAX deliveries accelerate in Sept. ‘19) and allows us to maintain consistent growth through FY20.

AGB & Labs:

Year 4 of AGB is under way. In May we launched flight connections at Rome Fiumicino, and in July extended it to Milan Bergamo. We have started selling Air Europa long-haul flights from Madrid on our website and have become the exclusive airline partner of the EU Erasmus Student Network. This partnership will enable Erasmus students to benefit from exclusive flight discounts to suit their budget and will be available from Aug. From June, our customers who purchase reserved seats now enjoy a 60-day check-in window. On Ryanair Rooms, we added a 5th partner, increasing both choice and value for our customers. Ryanair Holidays continues to roll out across our network and went live in Italy and Spain in Q1.

We continue to invest heavily in Travel Labs, and recently opened our 3rd Lab facility in Madrid which will see us hire up to 250 highly skilled digital professionals in Spain over the next 2 years. This follows on from the doubling in size of the team in Travel Labs Poland to almost 200 IT professionals earlier this year.

Our industry leading on-time performance improved in Q1 to 89%. We work hard to ensure that our customers enjoy punctual flights and we continue to campaign with our partners in A4E (Airlines for Europe) to encourage the EC to take action to ameliorate the impact of ATC strikes on overflights in Europe.

Costs:

The cost gap between Ryanair and competitor airlines continues to widen. We delivered a 6% unit cost reduction in Q1 as our fuel bill fell despite a 12% increase in traffic. Ex-fuel unit costs, helped by weaker sterling (which will, we believe, be reversed in H2 due to more difficult y-o-y comparisons), fell by 3% as we delivered unit cost reductions across nearly all cost lines. We remain on-track to deliver our previously guided ex-fuel unit cost reduction of 1% in FY18.

Our FY18 fuel is 90% hedged at approx. $49pbl and will deliver significant savings this year. We took advantage of recent price dips to increase our H1 FY19 hedging to approx. 45% at $48pbl. We expect these fuel savings will be passed back to Ryanair customers through lower fares.

Brexit:

We remain concerned at the uncertainty which surrounds the terms of the UK’s departure from the EU in March ’19. While we continue to campaign for the UK to remain in the EU Open Skies agreement, we caution that should the UK leave, there may not be sufficient time, or goodwill on both sides, to negotiate a timely replacement bilateral which could result in a disruption of flights between the UK and Europe for a period of time from April ’19 onwards. We, like all airlines, seek clarity on this issue before we publish our summer 2019 schedule in the second quarter of 2018. If we do not have certainty about the legal basis for the operation of flights between the UK and the EU by autumn 2018, we may be forced to cancel flights and move some, or all, of our UK based aircraft to Continental Europe from April ’19 onwards. We have contingency plans in place and will, as always, adapt to changed circumstances in the best interests of our customers and shareholders.

Balance Sheet & Shareholder Returns:

Ryanair’s balance sheet remains one of the strongest in our industry. In May the Board approved a €600m ordinary share buyback programme. In Q1 we spent €165m under this buyback at an ave. price of €18.20. We also purchased €39m worth of ADR’s under the €150m “Evergreen” ADR buyback programme launched last Feb. Despite this cumulative spend of over €200m on buybacks and capex of almost €400m in Q1, we reduced net debt by €150m from €244m at Mar. 31 to €94m at Jun. 30.

Outlook:

As previously guided, Q1 results were substantially boosted by the presence of Easter in April but not in the prior year comparable. While the H1 outcome remains dependent on close-in Q2 summer bookings, we continue to guide H1 ave. fares down approx. 5% as we grow H1 traffic by almost 11% and checked bag revenue continues to steeply decline. Thanks to the higher Q1 load factors and the completion of our winter ’17 schedule, we are raising our FY18 traffic target to 131m (up 1m on previous guidance). After a difficult winter last year, we expect the pricing environment to remain very competitive into H2 where we will grow traffic by approx. 7%. Yield visibility into H2 is zero and we see no reason at this time to alter our H2 ave. fare guidance of an 8% decline.

Ex-fuel unit costs are on track to deliver a 1% reduction this year, and our fuel hedging should deliver savings of approx. €70m, when adjusted for volume growth, which is being passed on to customers in lower fares. Ancillary revenue continues to grow in line with traffic as we discount pricing to drive penetration in products such as Ryanair Rooms, Ryanair Holidays and the PLUS bundles (which are reported in scheduled revenue).

Based on the above, we continue to guide FY18 PAT in a range of €1.40bn to €1.45bn. This guidance remains heavily dependent on close-in summer bookings, H2 ave. fares, and the absence of any further security events, ATC strikes or negative Brexit developments.”