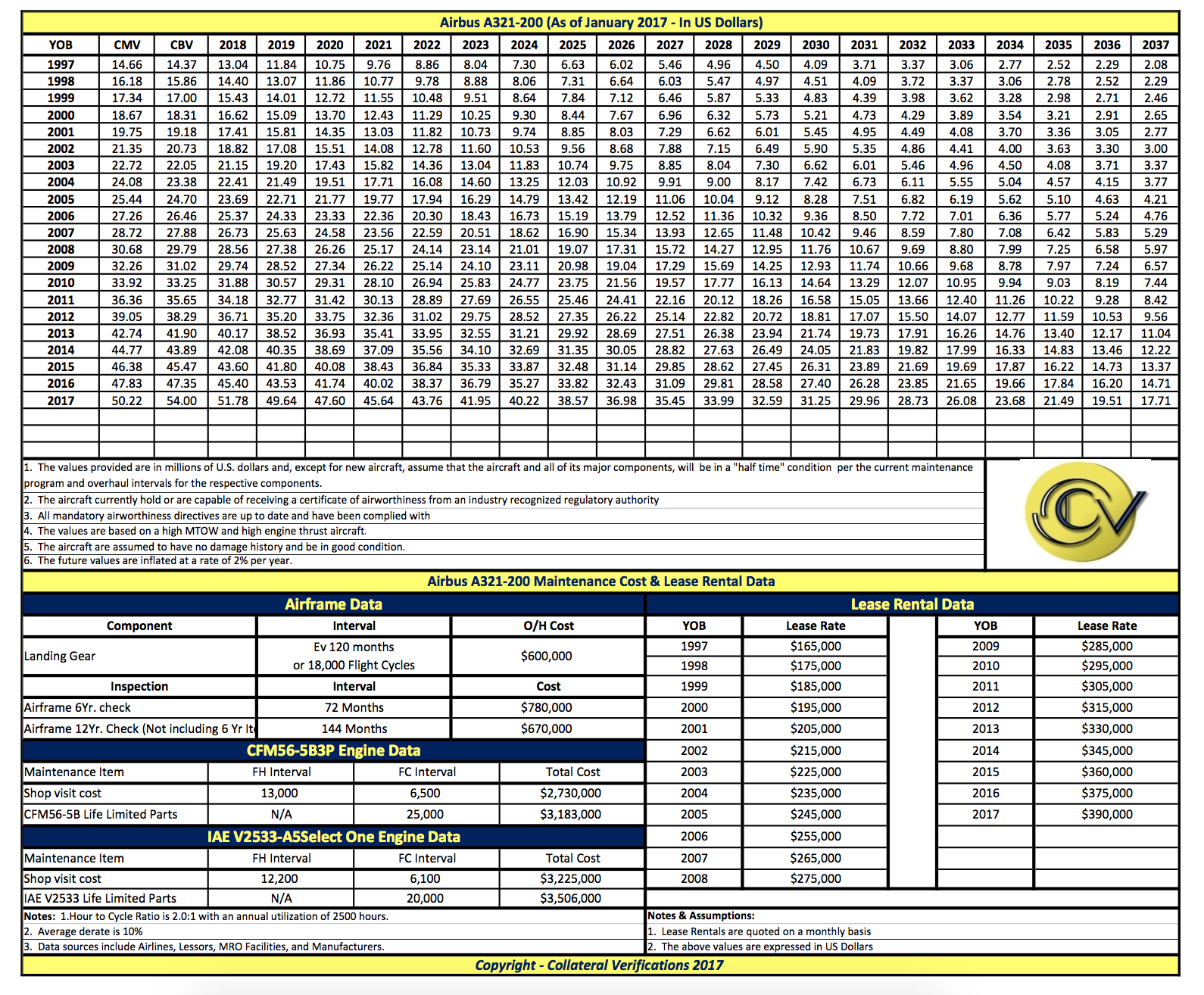

AIRCRAFT DATA

AIRCRAFT MARKET SUMMARY

The Current Market

The current market demand for new Airbus A321–200 has remained strong over the last 12 months. With the global demand for air travel coming back, in certain regions, operators are finding the capabilities of the A321 very attractive which has led to the continued stability of the type in the current environment. Today, CV knows of only 2 aircraft available for sale and/or lease. Out of more than 1,345 aircraft built, 27 are currently in storage, which is just under 2% of the current fleet. It is CV’s opinion that these percentages are considered low for a narrowbody aircraft type that has been in production for over 20 years.

Current values and lease rates in today’s market have remained stable for new and newer aircraft. This trend continues to show some signs of stability, due to the strong demand for the aircraft, which is expected to continue over the next 6–12 months. Based on this demand, we see values and lease rates for this aircraft remaining stable over the next 12 months with a potential for further recovery thereafter.

CV believes that the A321–200 with its quiet wide cabin, offering strong customer appeal, containerized cargo, commonality with other Airbus products, competitive choices of engines, fly-by-wire advantages, and being a part of a family of narrowbody aircraft, will keep this aircraft in good demand well through the rest of this decade.

The Competition

The A321 operates in the scheduled markets (typically 185 seats) and charter markets (220 seats high density), with its traditional rival, the Boeing 757–200, now having ceased production. The A321 has the advantage of being part of a family, offsetting the 757’s higher seat count and longer range. Boeing has now the 737–900ER to compete more closely, especially in the charter market, with the capability to carry 215 passengers. The A321–200 also looks a good longer-term prospect for freight conversion (joining the A320), once values fall to sufficient low levels; this is likely to be post 2016. The Airbus A321NEO and Boeing 737MAX will most likely put some pressure on the existing A321 products in the second half of this decade but the magnitude of the potential impact this may have is yet to be determined.

VALUE DEFINITIONS

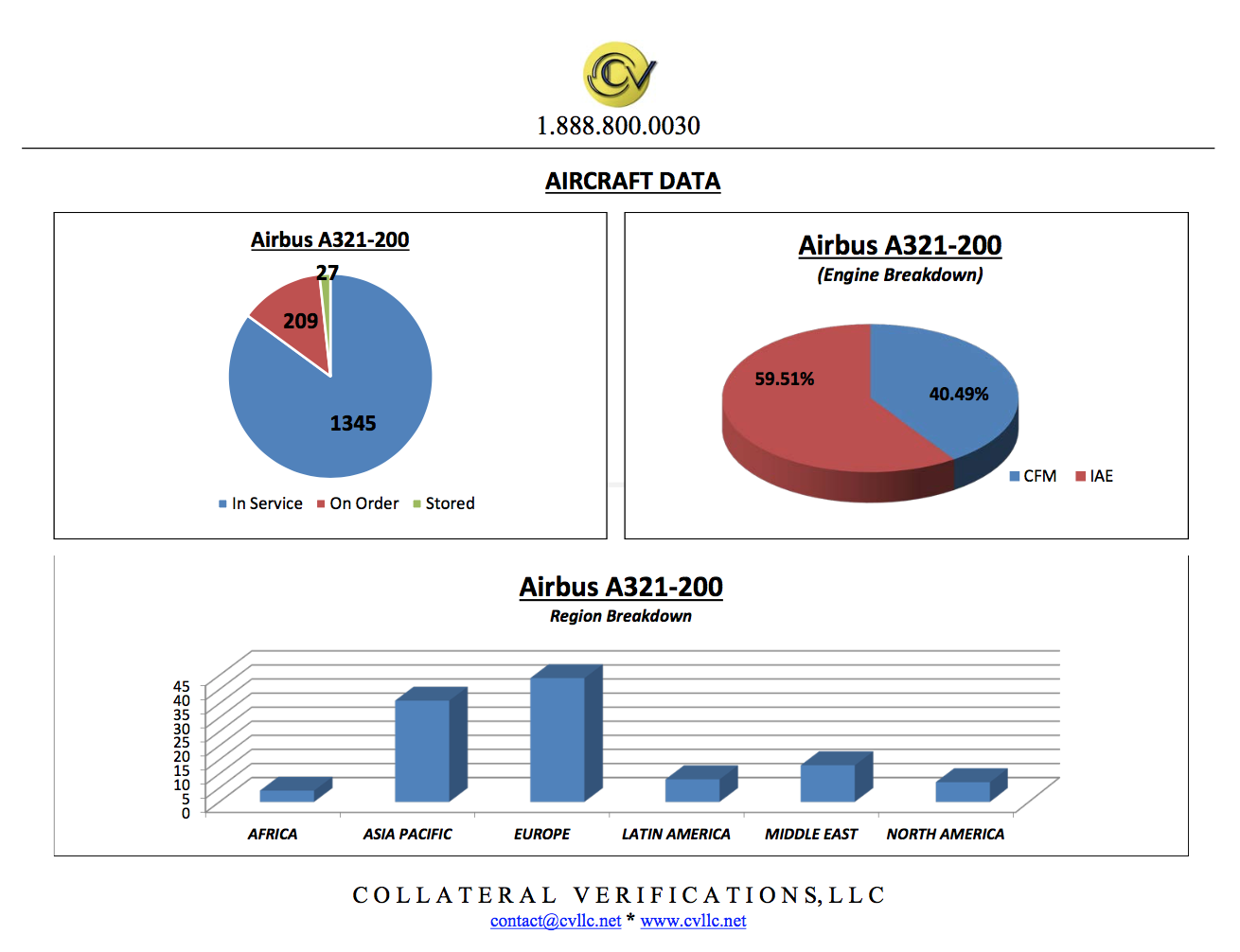

Current Market Value (CMV):

The Current Market Value (CMV) of an aircraft is the appraiser’s opinion of the most likely trading price that may be generated for an aircraft under the market circumstances that are perceived to exist at the time in question, according to the International Society of Transport Aircraft Trading (ISTAT). The current market value assumes that the aircraft is valued for its highest and best use, that the parties to the hypothetical sales transaction are willing, able, prudent and knowledgeable, and under no unusual pressure for a prompt sale, and that the transaction would be negotiated in an open and unrestricted market on an arm’s length basis, for cash equivalent consideration, and given an adequate amount of time for effective market exposure to perspective buyers.

Base Value (BV):

Base value is the appraiser’s opinion of the underlying economic value of an aircraft in an open, unrestricted, stable market environment with a reasonable balance of supply and demand, and assumes full consideration of its “highest and best use”. An aircraft’s base value is founded in the historical trend of values and in the projection of future value trends and presumes an arm’s length, cash transaction between willing, able and knowledge parties acting prudently, with an absence of duress and with a reasonable period of time available for marketing.

METHODOLOGY

Current Market Value (CMV):

To determine current market values of aircraft, CV uses, as our main source of data, any and all known reported market values. These values are extracted from numerous aviation industry sources and from CV’s proprietary and confidential transaction database.

As a secondary consideration, CV also analyses and gathers data on factors that influence the market value of an aircraft, such as its age, condition, configuration, fleet composition of such aircraft, similar aircraft available to the market, number of aircraft stored, operating economics, new aircraft prices, and the current state of the environment for the aviation industry.

This information is then entered into CV’s own proprietary transaction database and analyzed to determine a current market value based on a single sale transaction and using the assumptions as outlined in each aircraft valuation report at the time specified on the report.

Base Value (BV):

To determine its Base and Future values, CV first analyses any and all transaction information within its own proprietary database. This analysis allows CV to then establish the new price of an aircraft at a specific point in time. Historical data is then analyzed to determine the average depreciation rates of aircraft based on various conditions. This analysis is also broken down by aircraft type, mission, and in or out of production status. The result of these analyses is a depreciation factor which can then be applied to the various aircraft valuation models which CV utilizes for its valuation services and publications. Based on each valuation model, CV then creates base value curves for each aircraft which provide the base and future values for the aircraft which are reflected in the Turbine Aircraft Guide.

Lease Rentals:

The Lease Rentals provided in each valuation report represent CV’s opinion of aircraft lease rates in today’s operating lease environment. These lease rates are derived from CV’s own proprietary transactions database which contains a wide range of lease transactions received from numerous sources within the industry. This data is then compiled to produce the lease rentals provided in each aircraft valuation report.

Maintenance Cost Data:

The maintenance cost data provided in the Turbine Aircraft Guide is information that has been collected from various industry sources such as maintenance publications, conferences, MRO facilities, manufacturers, and financial institutions. The data represents the current estimated maintenance costs for such aircraft based on the assumptions and conditions provided.

Statement of Independence:

The aircraft valuation reports provided in the Turbine Aircraft Guide represent the opinion of Collateral Verifications and are intended to be advisory in nature. Therefore, CV assumes no responsibility or legal liability for actions taken or not taken by the purchaser of the Turbine Aircraft Guide or any other party with regard to the data provided in each report. By accepting these reports, the purchaser agrees that CV shall bear no responsibility or legal liability regarding these reports. CV also states that these valuation reports have been independently prepared and fairly represents the aircraft and CV’s opinion of its values.