SEPANG, 24 AUGUST 2017 – AirAsia X Berhad (“AAX” or “the Company”) today reported its financial results for the Second Quarter (“2Q17”) ended 30 June 2017.

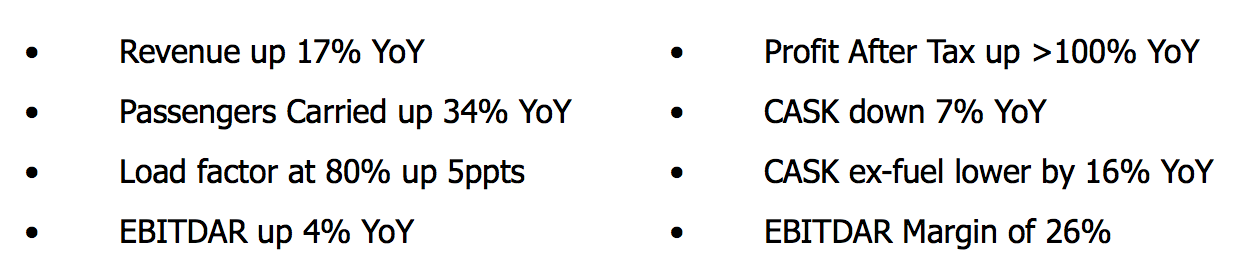

The Company recorded its seventh consecutive quarter profit with its RM47.4 million profit after tax recorded in 2Q17. Revenue grew 17% year-on-year (“YoY”) to RM1.0 billion mainly driven by the increase in passengers carried by 34% exceeding the 26% increase in seat capacity.

During the quarter under review, the Company recorded lower average base fare at RM455 in order to stimulate demand as can be seen by the significant increase in the number of passengers carried. Load factor was up 5ppts to 80% despite 26% capacity injection to 8,449 million against 6,682 million Available Seat Kilometers (“ASK”) recorded in the same period last year.

Revenue per Available Seat Kilometer (“RASK”) was down 7% YoY to 12.28 sen in 2Q17. The drop in RASK was due to increased capacity on existing routes resulting in lower yields. On the other hand, CASK improved 7% YoY to 12.32 sen while CASK ex-fuel improved 16% YoY to 8.13 sen, on the back of better cost efficiencies and higher aircraft utilisation.

AAX posted a net operating profit of RM3.8 million in 2Q17. Profit before tax for the period was RM27.9 million as compared to loss before tax of RM9.2 million in the same quarter last year. Net profit for the period was RM47.4 million as a result of foreign exchange gains and deferred tax recorded during the quarter.

AirAsia X Group CEO Datuk Kamarudin Meranun said, “We are pleased that despite challenging market conditions, we still managed to deliver the numbers in what was historically a lean quarter which again attests to the commercial viability of the long-haul low-cost model.”

“The second quarter for AirAsia X Malaysia has seen more ASK capacity injected as compared to the same quarter last year. This was to set the tone for future quarters especially the fourth quarter of 2017 and the first quarter of 2018, both historically strong quarters. While Australia remains Malaysia operations’ highest revenue contributor, China is fast catching up as we introduced Wuhan in first half of 2017 while adding frequencies on other China routes. Average base fare however, suffered from yield pressure as we increase capacity on core existing routes with our market dominance strategy. Our Malaysian operations reported EBITDAR margin of 26% and managed to pull in higher revenue of 17% YoY despite a competitive environment which proves that travel demand across our segments are still high.”

“AirAsia X Thailand performance has remarkably improved as compared to previous years’ second quarters. Thailand operations’ posted a strong 92% load factor, an increase of 3 ppts YoY, boosted by the 8% YoY increase of international tourists to Thailand in 2Q17 to 8.1 million. Revenue was up 28% YoY and passengers carried rose 26% YoY, exceeding ASK capacity growth of 21% YoY. We expect Thailand operations’ to extend its promising growth in the second half of 2017 as AirAsia X Thailand has been successfully recertified for its Air Operator’s Certificate (AOC) by Civil Aviation Authority of Thailand (CAAT) in June 2017. We hope that ICAO will remove the red-flag on Thailand soon as it will clear constraints restricting Thai-registered airlines from operating internationally, especially in countries which strictly abide by ICAO rules and regulations.”

“Meanwhile, AirAsia X Indonesia has successfully re-launched its A330s service in May 2017 with daily flights from Denpasar to Mumbai via Kuala Lumpur, and followed by the launch of Denpasar to Narita route. Despite just being slightly more than a month of re-launching A330 operations, AirAsia X Indonesia narrowed down its net loss for 2Q17 to USD3.8 million compared to USD9.8 million in 2Q16. We foresee an overall improvement from Indonesia in the coming quarters through greater operational synergies with AirAsia Group, especially AirAsia Indonesia.”

“Moving forward into the second half of 2017, the Group plans to re-strategise its position in Australia while focusing on the opportunities available from North Asia. The Group is also streamlining operations across the board to further unlock greater synergies with AirAsia Group. We expect this cost reduction initiatives will help us achieve up to 10% cost savings.”

“The Group looks to improve on its strategy of purposeful investment in securing high yield, high traffic routes and build market dominance in core markets across the region which will then drive competitive advantage with sustainable returns.”

Malaysia AirAsia X CEO Benyamin Ismail added, “The Company has delivered a commendable performance in a historically lean quarter with strong cost control and improving operational performance.”

“Revenue crossed the billion Ringgit mark for the first time in the Company’s second quarter history at RM1.0 billion, up 17% YoY. Scheduled flight revenue contributed 61% of total revenue, while ancillary revenue grew 41% YoY to RM193.5 million driven by the implementation of dynamic baggage and seat pricing, extension of in-flight entertainment availability to more routes, premium lounge and many more. In addition, it is also worth to note that our freight services recorded strong 27% YoY growth as we grow our cargo business.”

“Our load factor was up 5ppts YoY to 80% as we managed to stimulate demand and load across our market segments with our yield passive and load active strategy to tackle the lean travelling season. For instance, Australasia load was up 8ppts as we take lessons from previous years where we drove yield however our load lagged behind.”

“Our forward bookings are ahead of last year showing that demand to fly remains strong and reflects growing evidence that consumers are prioritising expenditure on flights and holidays above other non-essential items.”

The Company’s cost, measure in terms of Cost per Available Seat Kilometre (“CASK”) improved further in 2Q17. Benyamin highlighted, “I’m glad to report that CASK improved despite fuel prices have raised. This is mainly due to rigorous cost control and higher efficiency that was made possible with higher aircraft utilisation. I’m happy to note that aircraft utilisation has further been improved recently when we launched Kuala Lumpur-Denpasar short-haul route as we take advantage to maximise our day-time available window.”

On the balance sheet, Benyamin said, “The Management monitors the Company’s net gearing level closely to ensure that it is constantly at a healthy and comfortable level. At the end of 2Q17, the Company’s USD denominated borrowings has reduced by 9% from USD258.4 million in 1Q17 to USD235.7 million. The Company’s net gearing ratio therefore is at 0.61 times at the end of 2Q17, 13% lower compared to year end 2016 due to lower total debt.”